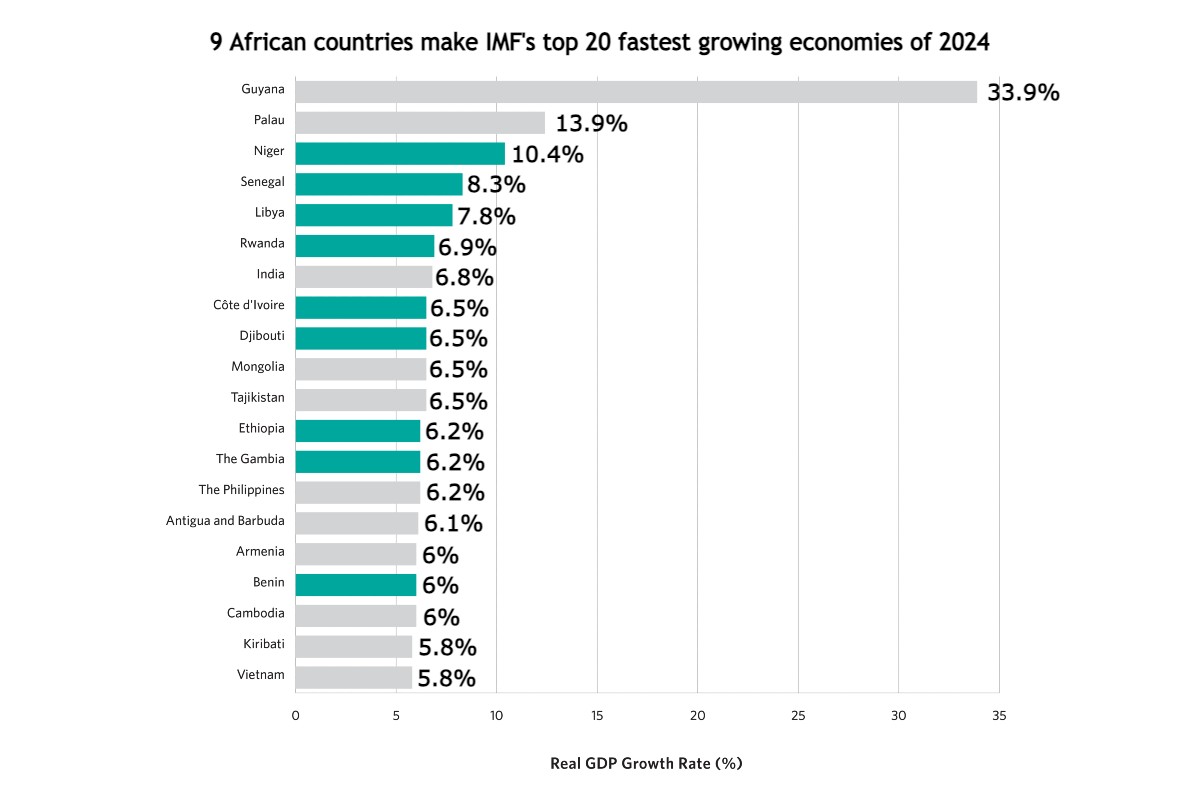

According to the IMF World Economic Outlook for April 2024, nine African countries are part of the top 20 economies in the world that are expected to have the fastest growth rates in 2024.

In general, sub-Saharan Africa is expected to experience a growth rate of 3.8 percent, which is higher than the global average of 3.2 percent.

This makes it the second-fastest-growing region in the world, right after Emerging and Developing Asia, which is projected to have a growth rate of 5.2 percent.

Here are the nine African countries with growth rates of between 6% and 11%.

Contents

1. Niger – 10.4%

Surprise, surprise. Niger is set to become not just the third-fastest-growing economy globally, but also the fastest-growing in Africa.

After a coup d’état in July 2023, Niger found itself on the receiving end of several economic sanctions imposed by the Economic Community of West African States (ECOWAS). In a show of solidarity with Burkina Faso and Mali, both of which were also under military junta-led governments, Niger made the decision to withdraw from ECOWAS as a form of protest against the sanctions.

Nevertheless, Niger boasts considerable oil resources, and the expected completion of a 2,000-kilometer pipeline linking Niger and Benin is projected to result in the oil industry accounting for a quarter of the nation’s GDP.

2. Senegal – 8.3%

Senegal, having recently overcome political instability, is poised to be the second-fastest-growing African economy, largely attributed to its rapidly developing hydrocarbons industry. The years 2014 to 2017 witnessed the discovery of over 40 trillion cubic feet of natural gas.

3. Libya – 7.8%

Projections indicate that Libya’s oil sector will continue to strengthen, boosting exports over imports and building up foreign reserves. The country’s oil output is expected to continue rising through to year 2028.

Despite this positive outlook, challenges like political instability and conflicts may lead to an oil blockade and increased humanitarian needs.

4. Rwanda – 6.9%

The tiny East African nation is set to leverage anticipated recovery in global tourism, along with new construction projects and a surge in manufacturing activities to sustain its economic growth.

Besides that, energy, mining, agriculture, trade and hospitality, and financial services are also key sectors of its economy. With a predominantly rural population, agriculture is a vital part of its economy.

5. Côte d’Ivoire – 6.5%

The country’s economic growth is being driven by ongoing investments in network infrastructure, especially in the digital and transport sectors, as well as the utilization of new oil findings, all supported by careful macroeconomic strategies.

Being one of the largest producers and exporters of cocoa beans and palm oil, the economy remains sensitive to global price fluctuations of these cash crops.

6. Djibouti – 6.5%

With its prime location, Djibouti is well-positioned to tap into the growing global demand for transshipment and logistics services. Its status as a free trade zone in the Horn of Africa further boosts its potential.

Downside risks stem from slowing global trade and spillover effects from sustained domestic political instability in Ethiopia

7. Ethiopia – 6.2%

Ethiopia, the second most populous country in Africa, is home to over 120 million people. It has witnessed consistent growth, averaging around 10% annually for the past ten years. This remarkable progress can be attributed to the thriving agricultural sector and the support received from foreign development aid.

However, Ethiopia is currently dealing with significant macroeconomic challenges such as an overvalued currency, increasing import costs, high inflation rates, and dwindling foreign exchange reserves. Both fiscal and current account deficits have been expanding, particularly following the conflict in northern Ethiopia.

Despite years of sustained growth, Ethiopia’s GDP per capita remains one of the lowest globally.

8. The Gambia – 6.2%

Spanning 450 km alongside the Gambia river, the country is encircled by Senegal, except for a 60-km stretch of coastline along the Atlantic Ocean.

The key factors behind the growth of real GDP in 2024 will be the strong inflow of remittances and the recovery of tourism, contributing to increased private consumption and investment.

9. Benin – 6%

The economy of Benin is set to grow, with real GDP forecasted to rise by an average of 6% between 2024 and 2027. This growth will be driven by public investments, donor support, and government reforms aimed at stimulating private-sector expansion.